Thai and International Taxation

Thai Taxation Overview

Monthly Thai Taxation Reporting Requirements

Corporate Income Tax in Thailand

Thai Corporate Tax

Thai Personal Income Tax

International Tax Planning

H. Toosi International Law Office offers clients taxation services and advice on a monthly, semi-annual and annual basis in compliance with Thai and international taxation and related regulations.

Our firm also helps clients to write legal agreements and contracts that lawfully minimize taxes. Services include professional help with the following arrangements relating to benefit entitlements:

1.Tax-free arrangements and transactions

2.Tax abatement arrangements and transactions

3.Arrangements and transactions in connection with an increase or decrease in depreciation of assets.

4.Agreements and transactions related to tax returns, overdue tax and late declarations.

5.Agreements regarding transaction tax (multiple taxation) and tax credits

We also provide legal advice on capital gains tax, wealth tax, inheritance tax and double taxation agreements.

H. Toosi’s advice concerning tax arrangements in Thailand:

Before entering into any business arrangements, small or large, ensure that you fully understand both the taxes you will be liable for and the tax protection you might be able to enjoy.

Thai Taxation Overview

In Thailand, taxes are based on taxpayer categories rates and tariffs, as prescribed by related tax laws, decrees and regulations.

The principal taxes in Thailand include direct taxes (personal income tax, corporate income tax, petroleum income tax) and indirect taxes (value added tax, specific business tax, customs duty, excise tax, stamp duty, property tax).

The Revenue Code, the main tax law in Thailand, deals with personal income tax, corporate income tax, VAT, specific business tax and stamp duty. The Petroleum Income Tax Act covers tax on oil and gas concessions. The Customs Act includes imports and exports, while other legislation governs excise tax and property tax.

Local administration authorities also collect property and signboard taxes.

Tax collection is the responsibility of the Ministry of Finance, operating through three (3) departments, and various local authorities.

1.Revenue Department collects corporate and personal income taxes, VAT, specific business tax and stamp duty

2.Customs Department is responsible for import and export duties

3.Excise Department looks after excise taxes on certain luxury commodities

4.In addition, municipalities (and Tambon Local Administrations) collect taxes on land, buildings, and signboards, where applicable.

Monthly Thai Taxation Reporting Requirements

H. Toosi helps clients follow Civil and Commercial Code requirements for maintaining financial records. This includes a number of monthly reports and payments that must be sent to the relevant Revenue Office.

1.Personal income or payroll tax covering all company employees must be reported. Personal income tax for each month must be delivered by the 7th of the following month. For example, personal income tax on all salaries paid for November should be sent by 7 December.

2.VAT must be reported and include all sales and business transactions. Monthly VAT must be sent by the 15th of the following month. For example, by 15 December for all sales and business transactions completed in November.

3.Tax withheld at source must be reported by the 15th of each month for the previous month. For example, by 15 December for all sales and business transactions completed in November.

4.Monthly social security contributions and a report must be sent each month to any entity.

H. Toosi’s advice concerning Thai monthly tax reports:

If your office sends reports or pays taxes late, interest and penalties will be imposed. Because prompt tax payments will save money, ensure that your office, or the legal office helping you with these reports, prepares and submits the documents on time.

Corporate Income Tax in Thailand

A Juristic Person must pay corporate income tax based on its net profit and at a progressive rate affecting 15-20 per cent of the company’s annual net profit.

However, there are some exceptions to this rate. For example,

•Public Limited Company listed on The Stock Exchange of Thailand (SET) or the Market for Alternative Investment (MAI) can have a reduced rate

•A company/partnership’s amount of registered capital may yield a reduced tax rate

Corporate income tax must be reported two (2) times each business year.

The first report covers six (6) months business activity and must include an estimate of annual profits together with a payment based on this estimate.

The second report must include the firm’s annual balance sheet and income statement. It must be sent to the Accounting Business Division, Department of Commercial Registration, within one (1) month of the date of the balance sheet’s approval by the shareholder's meeting. A company filing these reports late may be fined up to THB 12,000.

A multinational company may decide to make its accounting period the same as its head office. Normally, in Thailand, the fiscal year is 1 January to 31 December. The first accounting period can be less than 12 months, should it be the firm’s first fiscal year, and should the company wish to use more suitable or useful accounting dates.

All financial records must be examined and certified by a Chartered Accountant of Thai nationality.

H. Toosi’s advice on Thai corporate income tax

All tax and VAT receipts and bills that you use for income tax purposes must include the full name and address of your company as appears in your legal documents. If your business card does not have the same information (e.g. it might not include a full address), it is not a usable tax receipt.

Thai Corporate Tax

Companies and partnerships in Thailand must pay corporate income tax on net profit earned from both Thailand and overseas (if any) operations.

Firms, including private and public limited companies, partnerships, joint ventures, and other entities specified by the Revenue Code, are required to pay corporate income tax.

A regional or representative branch of a foreign company is taxed only on income earned in Thailand (see 2.3.6 Additional Company Structures in Thailand).

The rate of corporate income tax an entity is required to pay is based on the Thailand Revenue Code.

Some provisions included in the Revenue Code are:

•accrued loss shall be subtracted from net profits over the following five (5) years

•employer’s contributions to a registered provident fund (retirement scheme) are deductible

•up to four (4) per cent of net profit can be used for gifts and donations to approved public charities, education and sports bodies

•depreciation of assets is based on cost and varies from three (3) to 20 years

•up to 0.3 per cent (to a maximum of THB 10 million) of gross sales or paid-up capital (whichever is greater) can be used as entertainment and representation expenses

•unrealised (not yet real) exchange gains or losses shall be included

•inventory is valued at cost or at market price, whichever is lower

•bonuses based on a percentage of net profit are not deductible

•tax penalties, extra charges and fines are non-deductible expenses

•capital gains are ordinary taxable income

Thai Personal Income Tax

Personal income tax must be paid by any person who lives in Thailand for one (1) or more periods totaling 180 days or more in any tax year. The tax year for personal income tax is the end of the calendar year (31 December).

A resident must pay tax on all income earned in Thailand and on overseas income paid in Thailand. A non-resident pays tax only on income earned in Thailand.

Personal income tax is calculated by subtracting all expenses and allowances from all income ranging from zero (0) to 35 per cent.

Personal taxable income in Thailand includes:

•employment and service income

•income from copyrights

•interest, dividends, and capital gains on sales of securities

•rental income

•professional fees

In addition, you will be allowed to deduct various expenses from your personal income tax, e.g. contributions to a registered provident fund, life insurance payments and interest on a mortgage.

In addition, the following personal allowances are permitted:

1.THB 60,000 for the taxpayer

2.THB 60,000 for the taxpayer's spouse

3.THB 30,000 for each child

4.THB 30,000 for each parent

5.THB 60,000 for pregnancy and childbirth

6.THB 60,000 for disability

Other allowances:

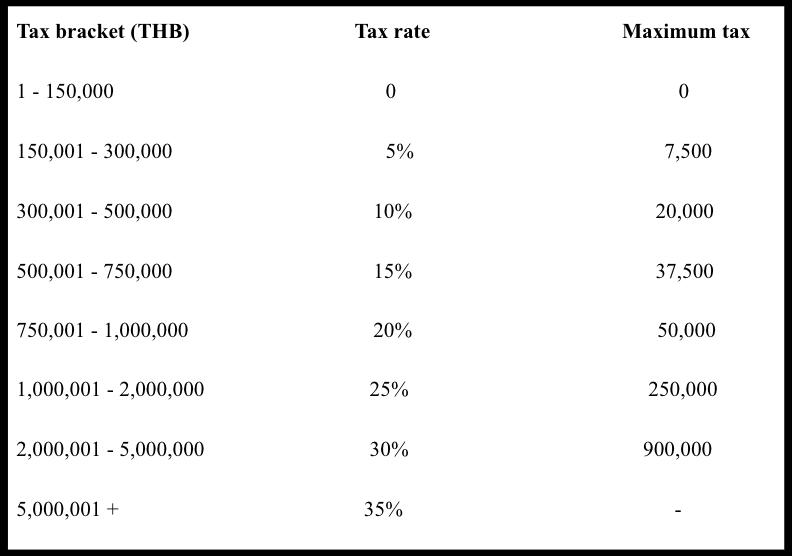

Tax rates

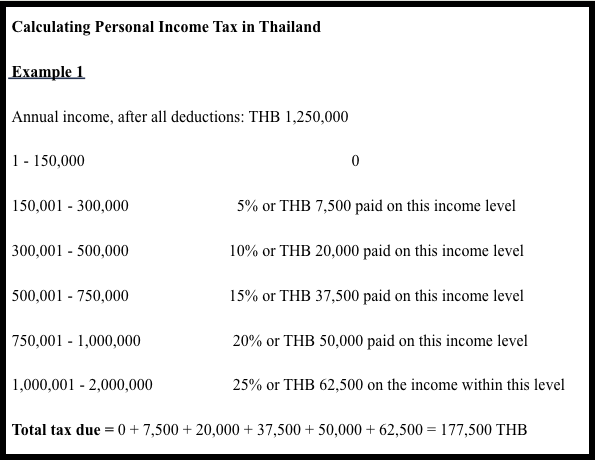

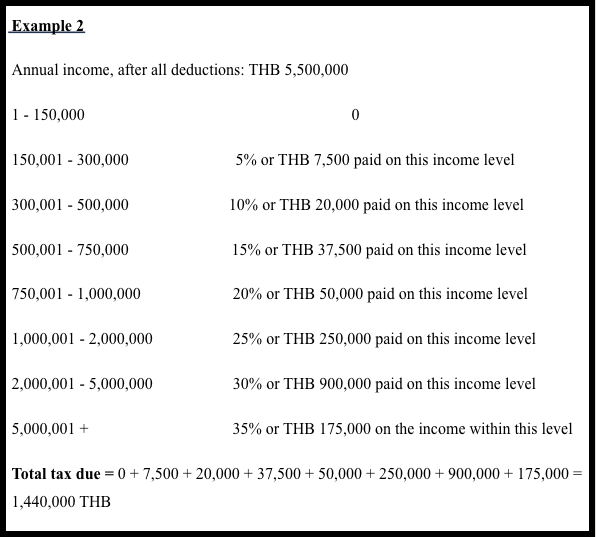

Thai personal income tax is based on eight (8) income brackets. Income is taxed at a flat rate within each bracket and added to the flat rate applying to the lower brackets (see examples).

International Tax Planning

International Withholding Tax and Double Taxation Treaties

Foreign companies that do not engage in business in Thailand but receive income from Thailand must pay international withholding tax. However, the tax rate depends on the double taxation treaty between Thailand and the company's home country.

A foreign company conducting business in Thailand may reduce Thai corporate tax liabilities by choosing an appropriate company structure. Therefore, it is important to know how to send profits out of Thailand legally and subject to the least possible tax. This requires an understanding of tax benefits, double taxation agreements, transfer pricing and offshore company arrangements.